Electric cars FAQ: frequently asked questions about EVs - from how much they cost to how long it takes to charge them

The UK Government has announced it is to ban the sale of new petrol and diesel cars by 2030 and hybrids by 2035, throwing the spotlight on electric cars as the future of driving.

Here we try to clear us some of the most common questions around EVs, ownership and costs.

What is an EV?

Advertisement

Hide AdAdvertisement

Hide AdAn electric vehicle (EV) is a car or van which is powered by electricity rather than traditional fossil fuel combustion engines. EVs drive their wheels via one or more electric motors, which are powered by large batteries. These are usually charged by plugging the EV into a purpose-built charging point.

They come in all shapes and sizes from city cars and family SUVs to supercars and cargo vans.

How much does an EV cost?

As with all cars, prices for EVs vary but they are, in general, more expensive than an equivalent petrol or diesel car.

Prices start at around £20,000, rising to well in excess of £100,000. A family hatchback such as the Nissan Leaf or VW ID3 starts at around £30,000.

Factors including the car’s size, battery capacity and motor power all influence the price of an EV.

Are there incentives or help to buy?

The Government currently provides a £3,000 plug-in car grant for buyers of brand-new EVs.

Some car makers also offer free or discounted home wall boxes for home charging.

Others have arrangements with energy suppliers that offer customers a set number of miles’ free charging each year or free or discounted access to public chargers.

How far can an EV travel on a single charge?

Advertisement

Hide AdAdvertisement

Hide AdMost new EVs have a real-world range of between 80 and 250 miles, depending on the model. Smaller city cars like the Smart EQ, Honda e or Seat Mii offer between 80 and 160 miles from their batteries but larger models such as the Kia e-Niro, Peugeot e-208 or Jaguar I-Pace have claimed ranges of between 230 and 280 miles.

Range is affected by various factors including where and how you drive, the weather and what in-car systems you are using.

Accelerating hard and driving quickly will harm an EV’s range, as will journeys in hilly areas.

Cold weather will also cut an EV’s range. Testing by the Norwegian Automobile Federation concluded that an EV will lose around 19 per cent of its WLTP range at temperatures between 2 and -6C.

While air conditioning will sap a little from an EVs’ range other systems such as lights and stereo have very little effect.

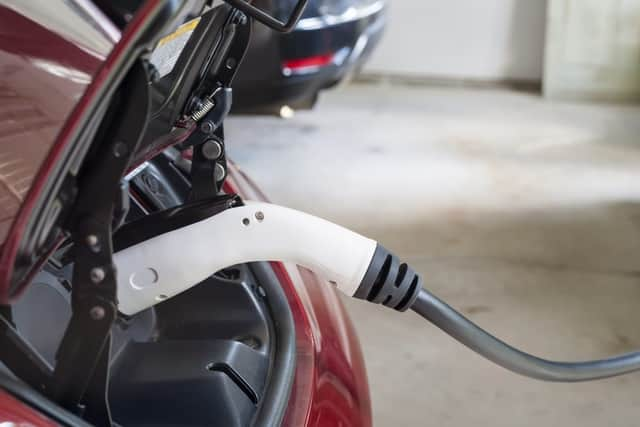

How long does an EV take to charge and how much does it cost?

Charging an EV can be done at home via a wall-mounted charging unit or at a variety of public charging stations.

Most home chargers operate at 7kW. To fully charge a 52kWh Renault Zoe from flat, a home charger would take nine to 10 hours, giving a maximum range of 242 miles. At the UK average electricity rate of 14.4p per kWh, that Zoe will cost £7.48 to charge.

Public chargers come in three main power outputs which offer different charging speeds - 7kW (slow) 22kW (fast) and 50kW (rapid). There are also some 100kW and 350kW chargers but these are relatively rare and not all cars can benefit from their additional speed.

Advertisement

Hide AdAdvertisement

Hide AdA 22kW charger will get the 52kWh Zoe from 0 to 100 per cent in two hours 54 minutes. On a 50kW charger, the 0-100 per cent time drops to one hour 29 minutes.

Charging costs at public points vary hugely. Some networks charge per kWh, others charge by time and some include an initial connection fee. An investigation by What Car? found prices ranging from 9p per kWh to 40p per kWh, with connection fees from zero to £3.50. On top of that, some services charge a monthly subscription.

Some supermarkets, restaurants and car parks offer free charging for customers and in Scotland ChargePlace Scotland offers unlimited free public charging for a flat £20 annual payment.

How much do EVs cost to run?

On top of charging you have other costs associated with running any car.

Car tax (VED) is free for zero-emissions cars, saving you £140 a year. And If you buy an EV as a company car you will pay 0 per cent benefit in kind in 2020/21 and one per cent in 2021/22. In comparison, a car emitting 100g/km CO2 is liable for a 22 per cent BIK rate.

EVs still need regular servicing but fewer moving parts mean there are fewer things to break and fewer consumables to replace, so maintenance should be cheaper than an ICE car.

Insurance, however, is more expensive for EVs. The exact difference will vary but comparison site Compare the Market found that EVs could be as much as 45 per cent more expensive.

How long do EV batteries last?

EV makers all offer a specific battery warranty with their cars. These are usually cover owners for seven or eight years and between 80,000 and 100,000 miles. This means that they expect the battery to still have at least 70 per cent of its usable capacity by that point. In practice, manufacturers such as Renault and Nissan have reported better-than-expected longevity and a study by Which? found that after five years the average battery still had 92 per cent usable capacity. Some estimates suggest EV batteries could last as long as 20 years before needing to be replaced.

Are EVs actually cleaner?

Advertisement

Hide AdAdvertisement

Hide AdIn terms of “tailpipe” emissions, yes. They produce no CO2 or other pollutants as they drive. However, if charged from nonrenewable energy sources, they still contribute to CO2 emissions.

Recent studies have found that, even when charged from nonrenewable energy sources, EVs are cleaner than an equivalent petrol or diesel car. Different studies have estimated that the CO2 emissions created by building and charging an EV over its lifetime are between 40 and 60 per cent lower than those produced in the manufacture and use of an ICE car. As the UK moves towards more renewable energy the CO2 impact of charging an EV will drop even further.

Can the National Grid cope?

Among the questions around charging EVs is whether the UK’s power supply could cope with the rapid wholesale adoption of electric vehicles.

According to Graeme Cooper, project director of the National Grid, the UK already has the capacity. He says: “Even if the impossible happened and we all switched to EVs overnight, we think demand would only increase by around 10 per cent. So we’d still be using less power as a nation than we did in 2002 and this is well within the range of manageable load fluctuation.”

However, when people charge their EVs could pose a bigger challenge, with sudden demand at the evening peak placing additional strain on the grid. It is hoped “smart charging” that can schedule charging for lower-demand periods such as overnight could alleviate this.